Moberg Pharma: Model of Europe Expanded

Moberg Pharma: Model of Europe Expanded

How to Be a Fungus Baron, Part 1A

Please read Part 1 before continuing if you have not already.

I have received two main questions on my model of Europe, so I will briefly address those here.

From Part 1:

Model Assumptions:

10% prevalence (probably low, large-scale studies suggest 14% in Italy and 13.8% in the U.S. with prevalence trending higher).

The 6 countries with Rx approval will switch to OTC approval as real-world data on the product becomes available.

No inclusion of the U.K., Germany, or other European markets to be pursued later.

An average of 4 infected nails per patient (the mean number of infected nails was found to be 4.4 in a Polish study).

An average of 0.03 ml of product per nail per day from a 5 ml tube.

270 million total inhabitants across the 13 approved countries.

48-week treatment course with once-daily applications (8 units per treatment course on average).

$3M in annual opex based on Q1 2024 opex, annualized and rounded up.

Corporate tax rate of 20.6%.

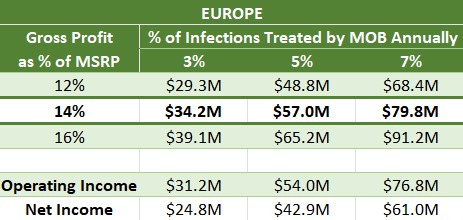

Why did you take 14% of MSRP as your central case for a gross profit rate?

This rate is equivalent to a 14% royalty on the product sold at full price (399 SEK)—revenue to the company minus COGS.

The terms of the licensing deals have not been disclosed, but this is what we know:

The ex-factory price will be €15 (166 SEK at the time of writing) in Europe—the revenue split between Moberg, the partner, and COGS.

Gross margin is 60% in Sweden.

Sweden will have a slightly higher gross margin than RoE because Moberg is helping Allderma with marketing spend.

Given those knowns, I am assuming Europe will have an average gross margin of 50%, and I am assuming the gross profit split with Bayer will be even, which implies an even split between the three of 166 SEK.

55.3 SEK to COGS

55.3 SEK to Bayer

55.3 SEK to Moberg

55.3/399 = 13.9%

That is where the 14% comes from. I believe it passes the sanity check.

Why did you use 3-7% as a range for the rate of EU TAM capture for MOB?

In Part 1, I estimated treatment rates in prescription markets to be 3-5%. If Rx treatment rates translated one-for-one to OTC treatment rates, 3-7% would be a very aggressive range, requiring total market dominance plus treatment rate expansion.

However, OTC treatment rates should be markedly higher than Rx rates for the following reasons:

Most people are ashamed of their onychomycosis and would be more likely to treat it if they could skip a conversation with the doctor and get it straight off the shelf or delivered to their doorstep.

Compared to prescription drugs, OTC drugs have far less stringent regulations around advertising in the EU. You can market an OTC product.

There is potential for misdiagnosis by patients. "Only about half of nail problems labeled as being fungal infections actually are." A lab test or experienced doctor would identify these cases and prevent a prescription from being written, but a self-diagnosing patient might try an OTC treatment for anything that looks fungus-like. In effect, the OTC TAM is higher than the Rx TAM.

So, OTC jurisdictions should see higher treatment rates than 3-5%, but how much higher? It is impossible to say for sure, but there is one good OTC-switching comp with high-quality data that can give a rough idea.

In 1996, the FDA approved three nicotine replacement therapies for OTC sale, which were formerly prescription only. A 1997 study found that “use of the medications [had] increased by 152% compared with prior prescription use”. The same product had 2.5x better market penetration under an OTC regime.

If OTC treatment rates were 7.5%-12.5% for onychomycosis, a 5% market penetration rate for MOB-15 would represent a 40%-67% market share.

That is plenty doable for a treatment entering an OTC market with NO COMPETITORS THAT ACTUALLY KILL THE FUNGUS. All the fungicidal products are prescription-only. In Sweden, for example, the incumbent market leader was Nalox, which doesn’t contain a fungicide (e.g., terbinafine or efinaconazole).

In one month of advertising, Terclara became the market leader at 36% share and drove 52% market growth YoY. There is no competition in OTC markets.

I believe Moberg should comfortably be able to treat 3-7% of onychomycosis cases in OTC markets.

Remember, Europe is just a piece of the puzzle, and if you can comfortably justify buying the company based on this geography alone, it qualifies as a “screaming buy”. We have yet to even touch the U.S., which will ultimately be the primary profit engine.

If you feel your time was well spent reading my work, please share.

Thanks for reading,

Sharpe

I hold a material investment in Moberg Pharma. My positioning may change at any time and without notice.

I do not work for the company in any capacity.

I write for informational purposes only; nothing written should be misconstrued as financial advice.

why do you think gross profit split b/w Bayer and MOB will be even? Thank you

Why do you go with the current label, as opposed to the US trial dosing regimen? (8 week daily + 40 week weekly application?)